10 Best Software Stocks to Buy in 2026

Over a decade in enterprise software taught me how these businesses actually work. Here's the watchlist, with the fundamentals and the charts that matter.

Most people come to software stocks backwards. They hear a ticker on a podcast, they buy it, and then they try to figure out what the company does after the fact. I did that for years before I learned a system. The order should be reversed. You understand the business, you understand the group it lives in, and then the chart tells you when.

So here are ten software names I think every investor should know in 2026. Some I own. Some I’ve worked at. Some I’ve pitched against in a deal. A few I’m watching and haven’t touched. For each one I’ll tell you what they do, give you the fundamental picture as it stands right now, and walk you through what I see on the chart.

A couple housekeeping notes. Several of these had earnings or corporate actions in the last few weeks, so the numbers below are current as of early June 2026. CrowdStrike has a 4-for-1 stock split effective July 2. Keep that in mind when you pull up the chart later this summer and the price looks a quarter of what you remember.

This is not financial advice. Please speak to a financial advisor before making investment decisions as they carry risk. I am simply a trader sharing his process.

Ok - lets dive in!

1. Snowflake (SNOW)

What they do: Snowflake is a cloud data platform. Think of it as the warehouse where a company keeps all its data, except the warehouse lives in the cloud and scales instantly. When Snowflake IPO’d it was the talk of every SaaS company in the country. Everybody knew somebody who got stock and woke up rich. It earned that hype because it solved a real problem for builders. It’s a platform for developers and data teams, a toolbox rather than a plug-and-play app, and that’s exactly why it stuck.

The fundamental brief:

Product revenue grew 34% year over year in the most recent quarter, an acceleration from 30% the quarter before. That reacceleration is the whole story here.

Net revenue retention sits at 126%, meaning existing customers spend 26% more each year. That’s the engine of a great consumption business.

Over 13,600 accounts are now using Snowflake’s AI features, and management is positioning the platform as the data foundation underneath enterprise AI.

Remaining performance obligations (contracted future revenue) are over $9 billion, so the demand is visible, not hoped for.

Still expensive on traditional metrics, which is the tax you pay for owning a fast grower at scale.

What the chart says: Strong reaction off earnings, now consolidating. It’s pulled back into the lows of the earnings gap-up and needs time. This is a big move digesting at its own pace. With the recent broad-market selling, the move now is to wait for it to go sideways and build something constructive before thinking about an entry. Not ruling it out at all. Just not ready.

2. Twilio (TWLO)

What they do: Twilio is a developer’s dream. Full disclosure, I own it and I used to work there. You create an account, connect a card, and use their APIs to wire your app into the phone network. Want your app to send a text or place a call? Twilio’s huge supplier network handles it through a few lines of code. They won the hearts and minds of developers the way the best infrastructure companies always do, by letting builders access powerful tools immediately without asking permission.

The fundamental brief:

Revenue grew 20% year over year last quarter to $1.41 billion, the fastest growth in more than three years.

Messaging growth accelerated to 25%, and voice grew 20% for the sixth straight quarter, both helped by new AI use cases.

Operating margin jumped to 7.7% from 2% a year ago. The profitability turnaround is real and showing up in the numbers.

Generated $132 million in free cash flow and bought back $253 million in stock during the quarter.

Management raised full-year guidance. The one watch item is gross margin pressure from carrier fees, expected to shave roughly 200 basis points this year.

What the chart says: Looks really strong. It broke out of a high tight flag, digested, and went first, ahead of most of the other software names. It digested beautifully, came off the 21-day EMA to new highs, and has been holding those highs well. This is a clear leader of the market and one of the strongest names on this list.

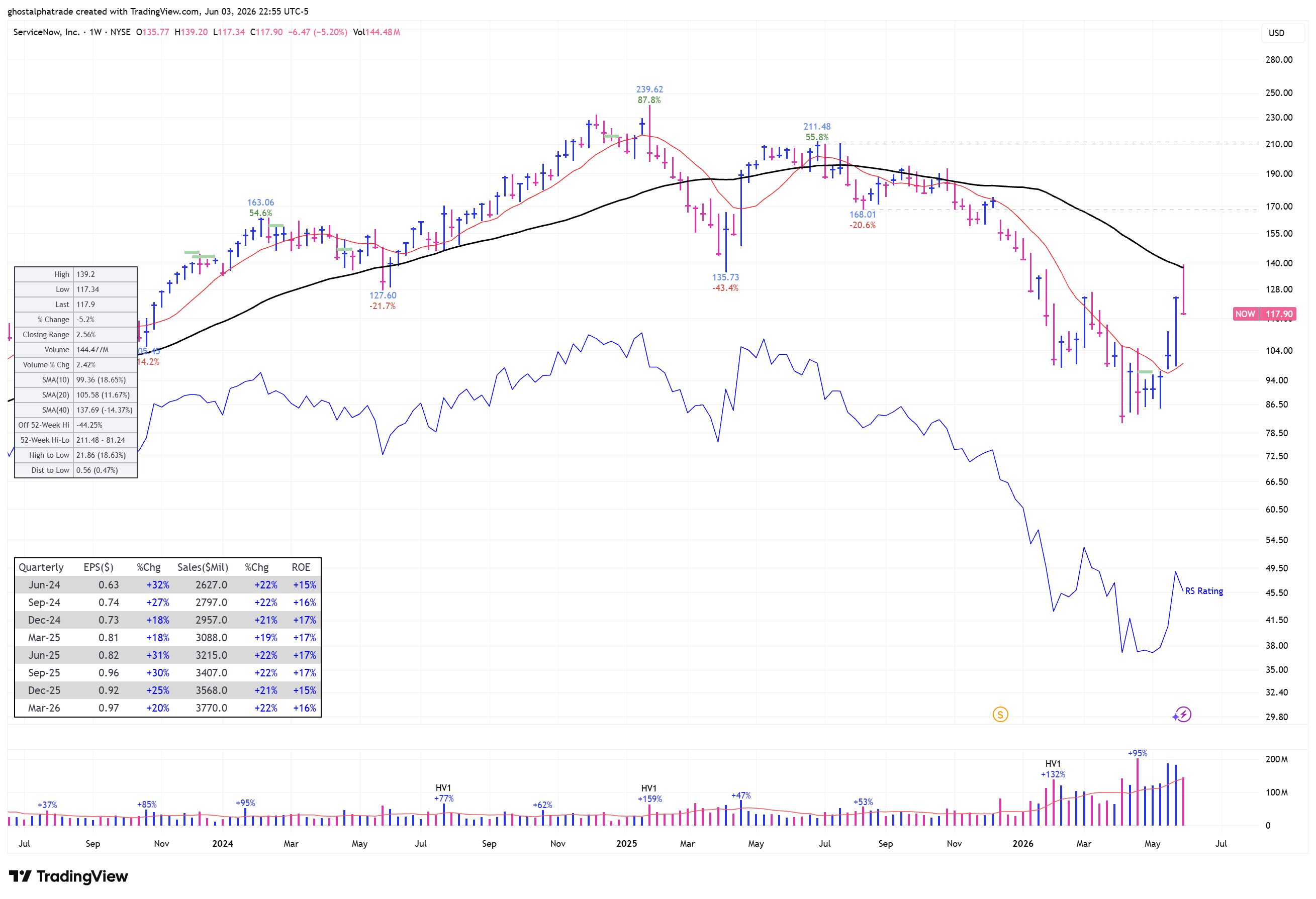

3. ServiceNow (NOW)

What they do: ServiceNow owns the IT service management space. If you’ve ever submitted a help-desk ticket at a big company because your laptop died, it probably ran through ServiceNow. They started in IT ticketing and have spent years pushing into adjacent workflows, taking shots at content management and other enterprise use cases. They’ve become a sort of platform for how large organizations get internal work done, and lately the market has treated the stock almost like a momentum name.

The fundamental brief:

Subscription revenue grew 22% year over year last quarter. At this size, that’s exceptional.

The AI product line (Now Assist) is the catalyst. Customers spending over $1 million a year on it grew more than 130%.

They run a “Rule of 55+” profile, meaning growth plus margin comfortably clears the 40 that defines a healthy software company.

Raised full-year subscription revenue guidance and authorized an additional $5 billion buyback.

Reminder: NOW completed a stock split, so the share price is far lower than the four-figure number long-time watchers remember.

What the chart says: Strong move right off the bottom, but it ran straight into resistance at the 200-day moving average. One of my hard rules is that I don’t buy stocks trading under their 200-day. So for now I’m watching to see if it can chop higher and eventually build a proper base. The business is dominant and the customer base is sticky, which is why it stays on the list, but the chart needs more work before it’s actionable.

4. CrowdStrike (CRWD)

What they do: CrowdStrike is cybersecurity, specifically endpoint protection and threat intelligence delivered from the cloud. They’re servicing one of the hottest areas in all of enterprise software right now. AI has made cybersecurity more important, not less, because the same tools that help defenders also help attackers. CrowdStrike has a strong brand and a deep customer base in IT security, and that matters in a category where trust is the product.

The fundamental brief:

Revenue grew 26% year over year last quarter to $1.39 billion. Annual recurring revenue crossed $5.5 billion.

Here’s the update to watch: CrowdStrike is now GAAP profitable, posting $27.8 million in net income versus a loss a year ago. Non-GAAP EPS rose to $1.10 from $0.73.

The earlier knock on this name was negative earnings. That story is actively resolving as profitability scales.

Management is guiding toward a long-term goal of $20 billion in recurring revenue and keeps raising the outlook.

A 4-for-1 stock split takes effect July 2, 2026. The chart will look very different after that, mechanically, not fundamentally.

What the chart says: Looks excellent. Broke out of a base, pushed above the 200-day, and everything is lined up: 10-day over the 21-day, 50-day over the 200-day. Strong move, then a few days of pullback that digested the gains well. I’d put it right next to Twilio in terms of leadership. The only thing that gave me pause was the earnings picture, because I buy fundamentals first and the chart second, never the other way around. With profitability now turning positive, that concern is fading.

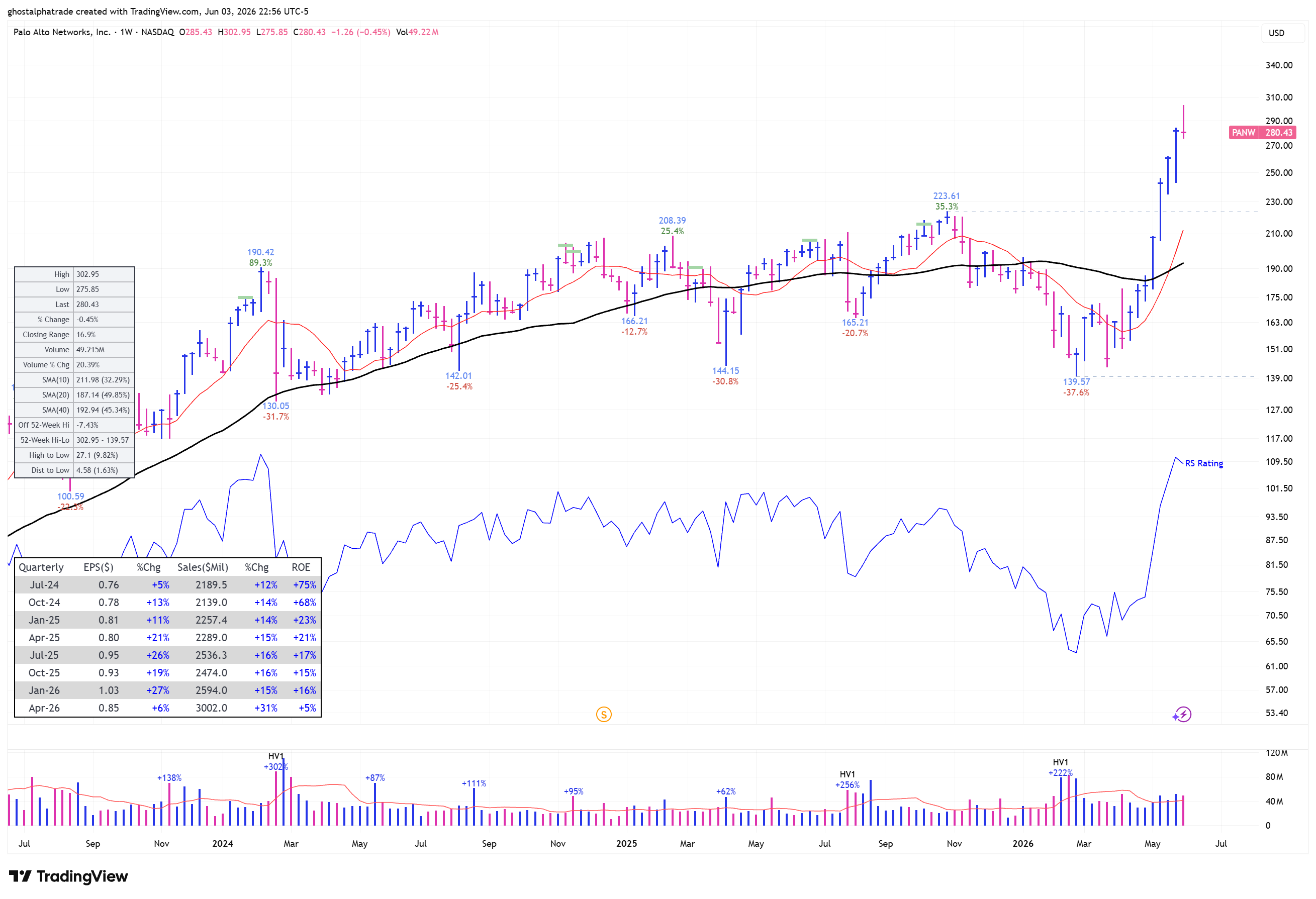

5. Palo Alto Networks (PANW)

What they do: Palo Alto is the other heavyweight in cybersecurity, with roots in network firewalls and a platform that now spans cloud security, identity, and AI protection. They’ve been around a long time and built a great name over those years, which counts for a lot in security. Same tailwind as CrowdStrike: AI has raised the urgency around protecting the enterprise, and Palo Alto sits right in the path of that spending.

The fundamental brief:

Just reported (June 2). Revenue grew 31% year over year to $3.0 billion, a real acceleration from the steady 12-to-15% range they ran for years.

That jump was helped by two big acquisitions, CyberArk and Chronosphere, expanding them into identity and observability.

Next-Generation Security ARR grew 60% to over $8 billion. That’s the part of the business the market cares most about.

Free cash flow grew 57% to $910 million. The cash engine is strong.

They posted a GAAP net loss this quarter on acquisition costs, but raised full-year earnings guidance, so the profitability trend is intact.

What the chart says: Looks a lot like CrowdStrike, almost identical. Strong move up, two days down, nothing wrong. A completely deserved pullback that’s digesting gains. Technically healthy. The sales reacceleration into the 30s is a genuine catalyst, and it shows up in both the numbers and the tape.

6. Datadog (DDOG)

What they do: Datadog is observability, the software that tells engineers whether their applications and cloud infrastructure are healthy. When something breaks at 2 a.m., Datadog is the dashboard that tells the on-call engineer where and why. I’ll be honest, I don’t have deep firsthand knowledge of the product, but I know the company hires extremely well. Some of the best salespeople I worked with at previous companies went to Datadog, and that tells you something about how they build.

The fundamental brief:

Revenue grew 32% year over year last quarter and crossed $1 billion for the first time. That’s the strongest growth in eight quarters.

AI workloads are now a real demand driver. Major hyperscalers are using Datadog to monitor GPU and AI training infrastructure.

Remaining performance obligations grew 51%, so future demand is highly visible.

Non-GAAP EPS of $0.60 beat handily, though GAAP net income is still thin at around $53 million. Worth knowing the gap between the two.

High-value customers (over $100K in annual revenue) grew 21% to about 4,550.

What the chart says: Looks good. Very strong recent move. I’m waiting to see if it builds a base and goes sideways for a bit before I’d act, but the fundamentals are among the most impressive on this list and the group it operates in is strong.

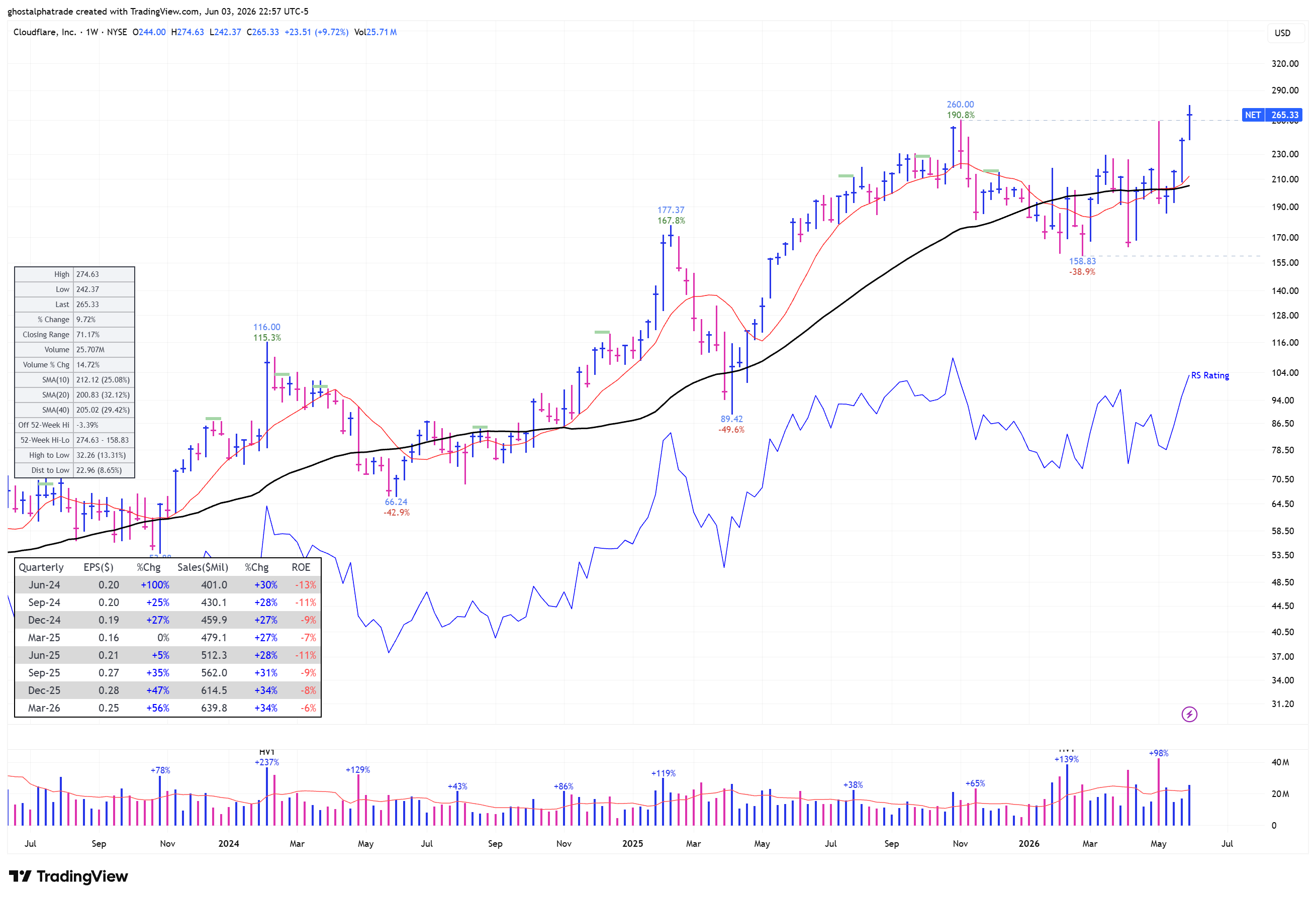

7. Cloudflare (NET)

What they do: Cloudflare serves a specific and important purpose. They’re network security and performance. When you run an enterprise, you want to protect your network, keep employees off dangerous sites, and stop attackers from getting in. Cloudflare sits in front of all that traffic. AI has scared a lot of people on the security front, and Cloudflare directly addresses that fear. Network security is its own niche inside the broader software group, and the people who work there tend to be specialists, not generalists. I went up for a role there once. They wanted people who understood the security space specifically, not just SaaS.

The fundamental brief:

Revenue grew 34% year over year last quarter to $640 million, with growth accelerating.

Deals over $1 million grew 73%, the fastest pace for that cohort since 2024. The enterprise is showing up in size.

42% of the Fortune 500 are now paying customers.

Here’s the news item: Cloudflare announced a roughly 20% workforce reduction (about 1,100 people) to shift to an AI-first operating model, with $140-$150 million in restructuring charges. Strong quarter, big internal bet at the same time.

Gross margin slipped to the low 70s as lower-margin developer and AI products grew. A trend to watch.

What the chart says: This one is interesting. It built a very long base, consolidating for over a year in a wide cup formation. It tried to break out to new highs in May, failed on a disappointing earnings report, and dropped hard, about 23%. It never quite cleared the old 260 highs. Then recently, off that low, it rallied impressively, pushed above 260, and has been digesting sideways above that level, which I think is healthy. From a relative strength standpoint it looks excellent. A lot of names got hit in the recent selling and this one barely shows a down day. Next to Twilio and Datadog, it’s taken the least damage. That kind of relative strength is worth paying attention to.

8. MongoDB (MDB)

What they do: MongoDB is a modern database. Traditional databases store information in rigid rows and columns, like a spreadsheet. MongoDB stores it in flexible documents, which developers love because it bends to how applications actually work instead of forcing the app to bend to the database. Their cloud product, Atlas, is the growth engine, and they’re increasingly positioned as a place to build AI applications on top of the data a company already runs.

The fundamental brief:

Revenue grew 25% year over year last quarter to $688 million, an acceleration from the 22% they’d run in prior years.

Atlas, the cloud product, grew 29% and is now at a $2 billion run rate.

The stock jumped more than 20% on this report and management raised full-year guidance.

Non-GAAP EPS of $1.32 beat by a wide margin. GAAP net income is still small, so mind the GAAP-to-non-GAAP gap here as with several names on this list.

Vector search and AI features are growing faster than the overall company, which is the forward-looking signal.

What the chart says: It looks like it’s forming a cup with handle. It’s early and still needs to digest, but if it can get back over 400, that becomes a meaningful level to watch for a potential entry. The distinguishing factor is that it’s actually building a pattern. I’d want to see the moving averages tidy up first, specifically the 50-day getting back above the 200-day. The 20%+ earnings pop is the kind of move that can resolve a base like this, so it’s firmly on the watchlist.

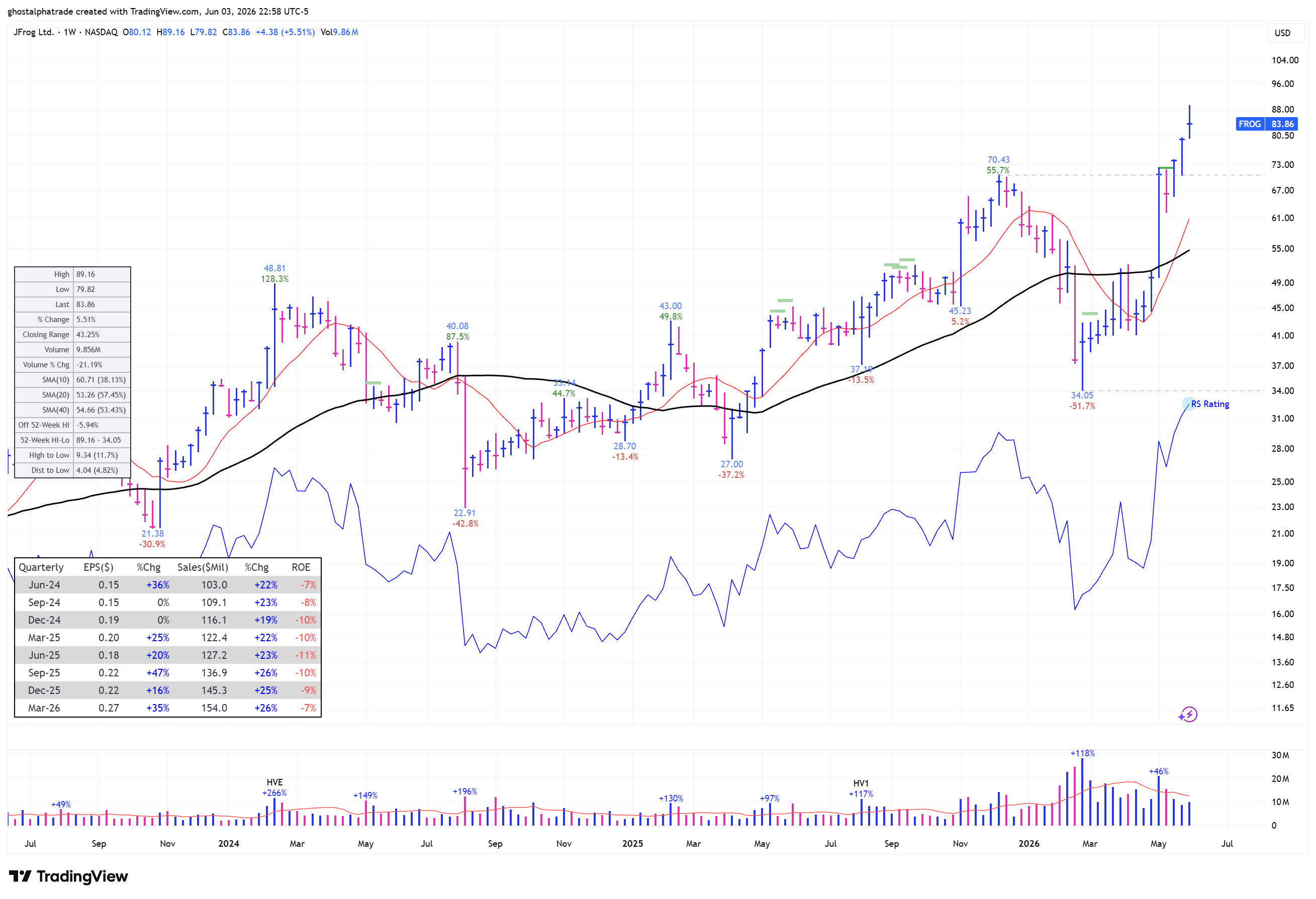

9. JFrog (FROG)

What they do: JFrog occupies a niche in software supply chain management. When developers build software, they pull in hundreds of outside components and packages. JFrog is the system of record that stores, manages, and secures all of those building blocks as they move from a developer’s laptop into production. It’s not a household name, and it was newer to me too, but the position they hold is mission-critical for the companies that use them.

The fundamental brief:

Revenue grew 26% year over year last quarter to $154 million, with cloud revenue up 50% and now over half the business.

Net dollar retention is 120%, improving, and gross retention is 97%. Customers stay and spend more.

Security and software-supply-chain attacks are a growing tailwind, which plays directly to what JFrog sells.

Like several names here, GAAP shows a small net loss while non-GAAP EPS is positive at $0.27. The cloud mix shift is the thing driving the model forward.

The board authorized a $300 million buyback, a sign of management confidence.

What the chart says: Really strong. It broke out of a high tight flag I was watching and digested the gains well. Everything is in order, all the moving averages lined up. This was one of my shortlisted names alongside Twilio and DigitalOcean. The combination of a clean technical setup and 26% growth with a 50% cloud business is exactly the kind of profile I look for.

10. DigitalOcean (DOCN)

What they do: DigitalOcean is cloud infrastructure built for simplicity, aimed at developers and smaller businesses rather than giant enterprises. Where the big hyperscalers can feel like flying a 747, DigitalOcean is designed to let a solo developer or small team deploy and scale an app quickly. More recently they’ve leaned hard into being an “AI-native cloud” built for inference and agentic workloads, which is their attempt to ride the AI wave without competing head-on with the giants.

The fundamental brief:

Revenue grew 22% year over year last quarter to $258 million, and they raised full-year guidance with 2027 growth now expected to exceed 50%.

Here’s the correction to my first read: this was a strong quarter. EPS came in at $0.44 against a $0.26 estimate, a roughly 69% beat.

AI customer ARR grew 221% and million-dollar-customer ARR grew 179%. The AI pivot is showing up in the numbers fast.

Adjusted EBITDA margin is healthy in the high 30s to low 40s. This is a profitable grower, not a cash-burner.

They raised equity and paid down debt during the quarter, strengthening the balance sheet for the AI buildout.

What the chart says: Technically strong. The flag was powerful, a jump from around 100 to a little over 160. It didn’t quite clear 100%, so it’s not textbook high tight, but it’s a strong move. When it broke out, though, it didn’t run far. It stayed right above its pivot rather than moving out quickly the way Twilio and JFrog did. That’s not necessarily bad, and it could still work. All the moving averages are in order and the relative strength looks good. I originally passed because my first read had the earnings going the wrong way. Looking at the actual numbers now, that was wrong, and this one deserves a fresh look. Early, strong, and worth watching.

How to use this list

You don’t need to own ten software stocks. You probably shouldn’t. The value of a list like this isn’t the ten names, it’s the habit. Pick the two or three that fit how you think, learn the business until you could explain it to a friend, and then let the chart tell you when the market agrees with you.

Right now most of these are digesting big moves. That’s not a problem, it’s a process. The leaders here (Twilio, CrowdStrike, Palo Alto, JFrog) have already shown their hand. The base-builders (Snowflake, MongoDB, Cloudflare, Datadog) are telling you to be patient. And a couple (ServiceNow, DigitalOcean) are puzzles I’m still working through.

The system doesn’t ask you to predict. It asks you to prepare. Build the watchlist now, so when the setup comes, you’re not meeting the company for the first time.

If this was useful, subscribe. I document the real trades, the real losses, and the real process, one week at a time.

Did I miss any?

Great article. Thank you!

Good read - I personally like DDOG and CRWD although both valuations are a little stretched now in my opinion. Outside of those, I'm keeping my eye on PCOR but mgmt turnover has me cautious.