Are You Still Watching? Netflix and Three Other Setups Ahead of a Critical Week

The market is on day four of a rally attempt. Here's what I have ready if it confirms.

Everything here is for informational purposes only. Do your own research, size your risk appropriately, and never trade money you can't afford to lose.

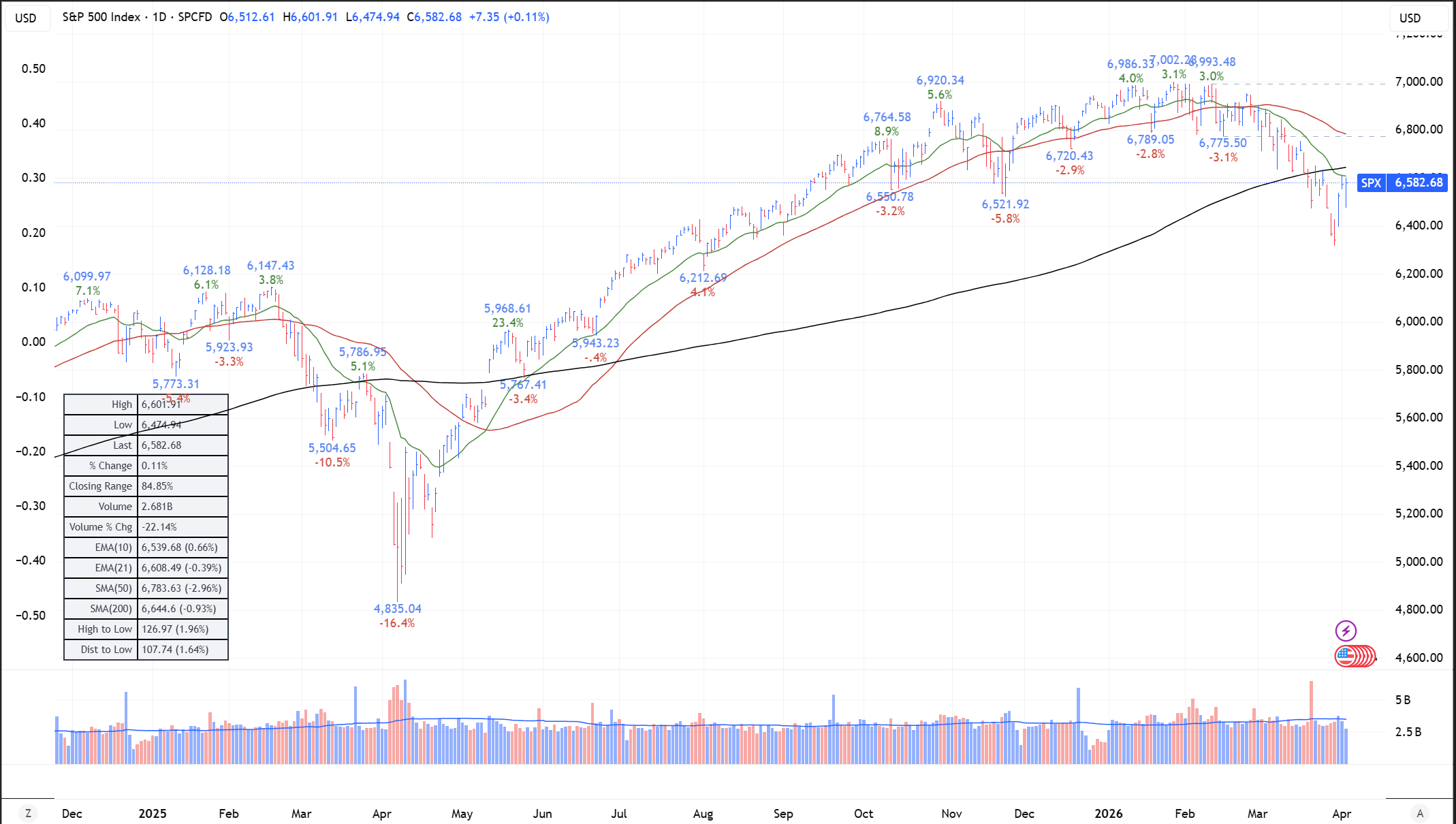

Right now, 80% of my account is sitting in cash.

That’s not panic. That’s the system working exactly as it’s supposed to.

We’re in a correction. The S&P is under pressure, the indexes are broken, and until we get a confirmed follow-through day, there’s no reason to be a hero. One thing I learned from studying O’Neil: you don’t have to be in the market all the time. Sometimes the best trade is no trade.

For anyone who hasn’t heard the term before, a follow-through day is how we know a rally attempt is the real thing versus a head fake. The rule is simple: wait at least four days off the bottom, then look for a big up day on heavier volume than the day before. That kind of price and volume action tells you institutions are putting serious money to work. Without it, you’re guessing.

Thursday was day three off the bottom. The market was closed Friday. That makes Monday day four, which means we could get a legitimate follow-through day right when the week opens. Historically the strongest ones come between day four and day seven, so we have a real window here.

In the meantime, here’s what I’m watching. These are the four setups I’ll be ready to move on if the market confirms.

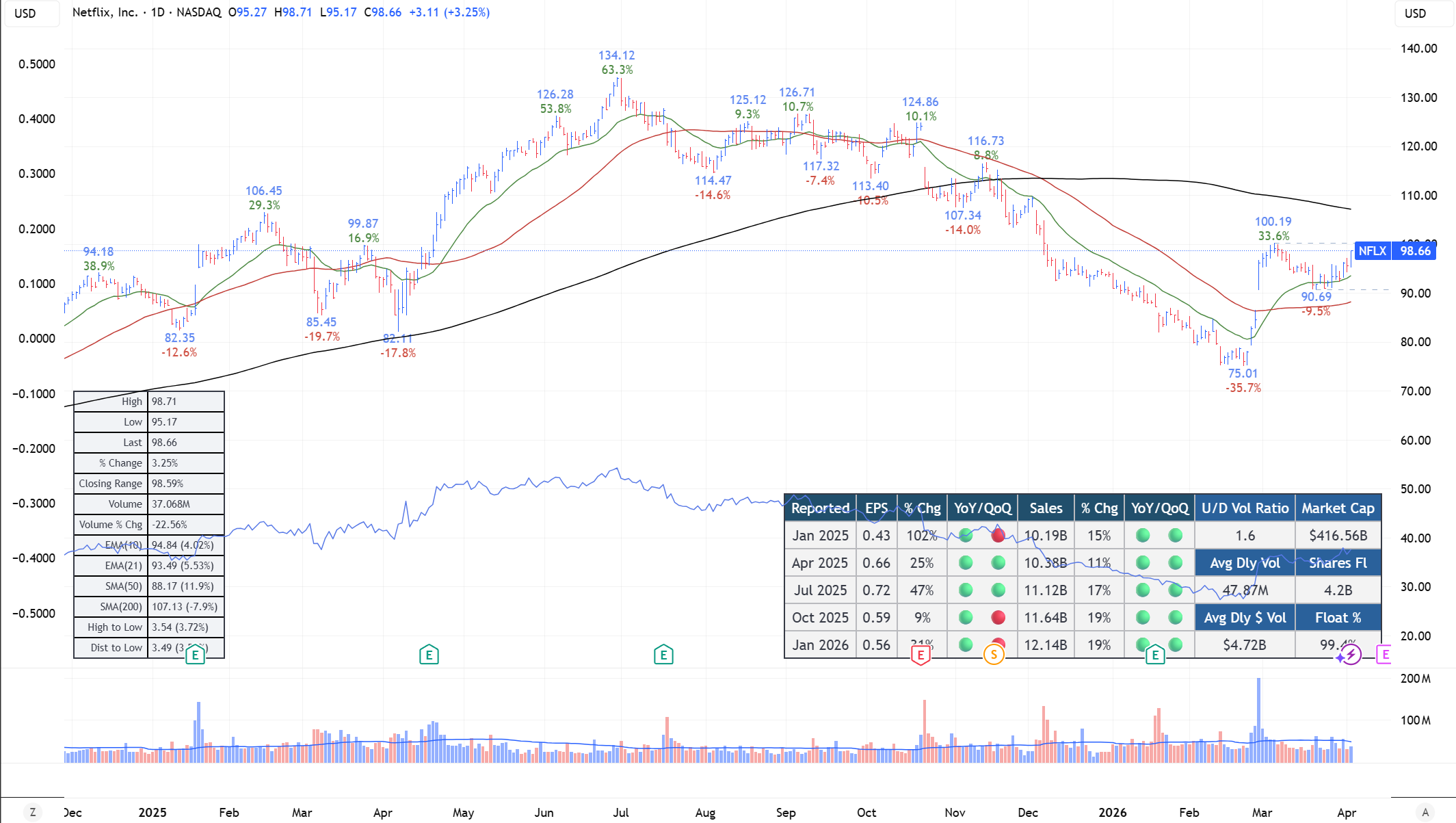

Netflix (NFLX)

Fundamentals

Earnings came in at 31% growth last quarter, just clearing the 25% threshold we look for. Sales growth was lighter at 19%, which is softer than ideal. We want to see 25%+ on both sides, and the best merchandise usually delivers 50%+. So the fundamentals here are a pass, not a conviction call, but they’re good enough to stay on the list given everything else happening with the company.

The story is genuinely interesting. Netflix just acquired InterPositive, an AI filmmaking tools company co-founded by Ben Affleck, for up to $600 million. The technology helps filmmakers work more efficiently in post-production, continuity fixes, scene enhancement, that kind of thing, and it won’t be commercialized externally. They’re building this in-house. At the same time, they just raised prices across all U.S. plans for the second time in less than two years, projecting ad revenue to roughly double in 2026 and targeting $20 billion in content spend. The company has pricing power. Not many businesses can say that right now.

Technicals

The chart had a rough stretch. After a strong run through the first half of 2025, it sold off hard, broke the 50-day, broke the 200-day, and spent months under both. Normally that’s a disqualifier. But look at what happened off the bottom.

It found support around $75, bounced hard to $100, and has been consolidating tightly in that range ever since. What’s forming looks like the right side of a cup. It could tighten into a handle from here, which would actually be preferred. Lower volume, some shakeout of the weak hands, then a clean breakout. There’s overhead supply to work through, but this stock has had plenty of time to digest it, and the volume on that $75 to $100 run was unusual in the best way.

Game Plan

Watching for a handle to form on lighter volume. Pivot point is around $98. A strong move through $100 on big volume works too. If I’m in and it breaks the 21-day moving average, I’m reducing. Hard stop at 5-8% below entry, no exceptions.

SanDisk Corporation (SNDK)

Fundamentals

This is the strongest fundamental story on the list.

Last quarter: 404% earnings growth, 61% sales growth. Those are the kinds of numbers that make you stop scrolling. The caveat is that it’s somewhat of a turnaround story. The prior quarters weren’t stringing together the kind of consecutive acceleration we’d ideally like to see. One monster quarter is a signal. Three in a row is a trend. We’re watching to see which one this turns out to be.

The story is the NAND memory cycle turning. Companies like SanDisk and Micron operate in a cyclical industry where pricing and demand swing hard in both directions. When the cycle turns up, and the data suggests it has, these stocks can move faster than almost anything else in the market. Storage demand tied to AI infrastructure is a real tailwind. This isn’t a company inventing a story. The demand is there.

Technicals

The chart is one of the most constructive on my list. After nearly tripling from the $284 area to almost $800, the stock has been digesting that run in what looks like a bullish flag. There’s also an argument for a double bottom if you look at it from a different angle. Either way, the structure is tight and orderly, the kind of price action that tells you institutions are holding, not distributing.

The RS line is strong, outperforming the S&P even while the broader market is in a correction. That’s leadership. When the market turns, stocks with RS lines like this tend to move first.

There was a failed breakout attempt at the $725 level on the first flag run. That matters. Now the stock has undercut that pivot, which can shake out the weak holders and reset the base. A second attempt through $725 on strong volume would be a compelling entry.

Game Plan

I wouldn’t wait for absolute new highs on this one. I’d start building a position as it approaches that $725 resistance on strong volume, then add if it breaks through to new highs. Moving averages are the guide for stops. If it breaks below with force, that’s the exit. 5-8% hard stop in place from the start.

Dell Technologies (DELL)

Fundamentals

Dell is not a small-cap momentum story. It’s a $100+ billion revenue company that has quietly become one of the most important AI infrastructure plays in the market.

Last quarter delivered 45% EPS growth and 39% revenue growth. That’s not a blip. It’s part of a multi-quarter trend. For all of fiscal 2026, Dell posted record revenue of $113.5 billion, record EPS, and record cash generation. Their AI-optimized server business grew over 300% year over year. They’re guiding for $50 billion in AI server revenue in fiscal 2027, roughly double what they just did. They have a $43 billion backlog going into this year. That’s not a company hoping AI demand materializes. That’s a company with the orders already on the books.

The story is founder-led stability meets the AI infrastructure supercycle. Michael Dell built this company in a dorm room. He’s been running it through every cycle since. That matters.

Technicals

The chart shows a long base, really from mid-2024 through now. A big gap-down in June 2024 started the consolidation, and the stock spent the better part of a year working through it. Choppy, frustrating action for anyone who was in it. But that kind of time in a base is actually constructive. It shakes out the impatient holders and resets the supply-demand picture.

Now it’s approaching the prior highs around $179.70. The left side of the base around $166 to $168 has already been cleared. The real question is whether it can push through those all-time highs and hold. I’d call the current setup a cup with handle in spirit. Not perfectly formed, but the structure is there.

One thing I’ll note: it’s a bit extended from its moving averages right now. Personally I prefer setups where the stock is basing near its 50-day. It gives me a cleaner stop and double confirmation when things go wrong. That said, this one is finding good support at the 21-day, so that’s the level to watch.

For the longer-term reader, this is also the kind of stock that works well alongside an index as a core holding. Big, liquid, growing. If markets stabilize, DELL is the type of name that benefits broadly.

Game Plan

Any clean break through $179.70 on strong volume is the entry. I’d be comfortable building a position in the current range too, given the cleared left-side resistance. 21-day moving average is the guide. Hard stop 5-8% below entry.

International Seaways (INSW)

Fundamentals

This one is a different kind of story, and that’s what makes it interesting.

International Seaways is a tanker company. It moves crude oil around the world on a fleet of roughly 70 vessels. Not a flashy business. But energy transportation is one of the strongest industry groups in the market right now, and that matters just as much as the company-specific story.

Last quarter delivered 172% earnings growth and 38% sales growth. Big numbers, and they came in ahead of what analysts expected. The honest caveat is that this is a cyclical, and tanker rates can swing hard. The prior history of fundamentals isn’t what you’d see in a software company with 10 years of consistent growth. That’s a real con against this setup. But when the cycle is moving in your direction and the chart confirms it, you work with what the market is giving you.

The story is geopolitics driving oil demand. Ongoing tensions in key shipping regions have kept tanker rates elevated. INSW sold five older vessels recently for roughly $185 million and is modernizing its fleet. They paid out a $2.15 per share combined dividend. The company is running well.

Technicals

The RS line is the best one on this entire watchlist. If relative strength is the measure of leadership, INSW is leading. The stock ran hard from April 2025 into recent months, found resistance around $78.51, and has been consolidating sideways since. It’s not a textbook cup. The consolidation is a little wide and choppy for that. Call it a sideways base. Not perfect, but functional.

What I like is the tightness of that consolidation relative to how far the stock ran. It digested a big move without giving much of it back. That’s strength.

Game Plan

The $77.70 area is where I’d start looking to build a position on any market confirmation. New highs above $78.51 is the cleaner breakout entry. RS line is the primary reason this is on the list. That kind of outperformance tends to persist when market conditions improve. 5-8% stop below entry, moving averages as secondary guide.

None of these are trades yet. They’re setups. Stocks that have done the work to be ready when the market gives us the green light.

The follow-through day is the gate. Until we get one, we wait. This is the part of the process most people can’t stomach, which is exactly why most people don’t make money in markets.

The discipline to sit in cash while good setups form in front of you is a skill. It took me years to develop it. But the setups that work best are the ones where you let the stock come to you, not the ones where you chase.

Stay patient. We’ll know more by the middle of next week.

If you found this useful, consider subscribing for weekly analysis. No noise, no hype, just the process