This Might Be Our 90's

The four biggest companies in the world just reported earnings. Here is what it means for the AI infrastructure trade.

There is a story I keep coming back to.

People who were paying attention between 1995 and 1999 talk about that period the way people talk about being at a great concert. You had to be there. The Nasdaq went up 400% in five years. Cisco, Intel, Microsoft. Companies that were building the infrastructure for a world that was just starting to come online. The internet was real, but most people were still figuring out what it meant. The ones who were watching the price action of the leaders knew before everyone else.

I think about that a lot when I look at what is happening in AI right now.

Tonight changes the narrative.

After the close on April 29, four of the largest companies on earth reported earnings. Microsoft, Alphabet, Amazon, and Meta. Together they have committed somewhere north of $650 billion in AI capital expenditure for 2026 alone. Tonight was the first real accountability test. Were the revenue and margins keeping pace with the spend?

The answer, mostly, is yes.

Microsoft reported revenue of $82.9 billion, up 18% year over year. Azure grew 40%. Their annualized AI revenue now stands at $37 billion, up 123%. Alphabet beat on revenue at $109.9 billion with Google Cloud growing at a rate analysts had been pricing in as a stretch. Amazon posted a strong beat across the board with AWS growing 28% to $37.6 billion. Meta beat on revenue and EPS, raised Q2 guidance to $58 to $61 billion, and told the market it is spending even more on AI infrastructure than it previously planned.

The market punished Meta after hours for the capex raise. The stock dropped more than 6%.

That reaction tells you everything about where we are in this cycle.

The noise versus the signal.

A few weeks ago, OpenAI reportedly missed its 2025 revenue targets. AI stocks sold off. The narrative that spread across every financial media outlet was simple: maybe AI is not working. Maybe the spend is getting ahead of the revenue.

I want to offer a different frame.

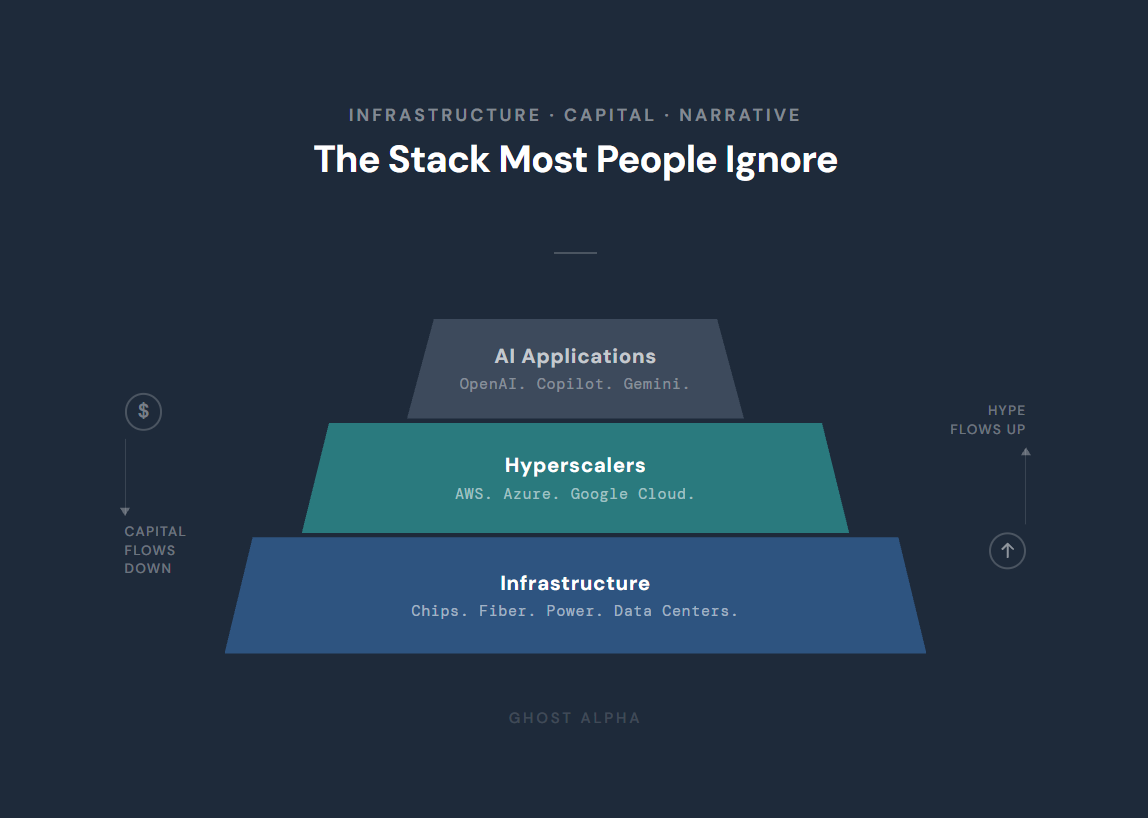

I spent years working in SaaS. Software as a Service is the layer most people think about when they think about technology. The application. The thing you log into. Salesforce. Workday. HubSpot. We are trained to evaluate technology at the top of the stack because that is where we interact with it.

AI is not the same.

OpenAI is a product. It lives at the top of the stack. But the infrastructure underneath it, the compute, the fiber, the data centers, the power, the chips, that is the real story. That is what Cisco was to the internet. And the hyperscalers, Microsoft Azure, AWS, Google Cloud, they are the ones building and monetizing that layer right now.

OpenAI missing revenue targets tells us something about consumer adoption curves at the application layer. It does not tell us anything about whether the infrastructure buildout is real.

Tonight’s earnings tell us the infrastructure buildout is very real.

What the price action is saying.

Here is what I keep coming back to as a trader. The market votes every day. And for the past several months, certain names have been standing out in a specific way. Relative strength versus the S&P 500, holding key moving averages while the broader market struggles, volume patterns that suggest institutional accumulation rather than distribution.

The universe of companies that sit inside this AI infrastructure theme, data centers, fiber optics, electrical components, energy, chips for compute, these names have been telling a story in the charts that is hard to ignore.

NVDA. Marvell. Nebius. Comfort Systems. Bloom Energy. Sandisk.

Not all of them are setting up right now. Some have broken down on earnings and needed to be cut. That is part of the process. But the ones that are holding, the ones that are building bases while the market figures out what tariffs mean and whether the Fed will move, those are the names worth watching.

The honest take.

I do not know if this is our 90s. Nobody knows that until it is over.

What I know is that every major technology cycle in history looked obvious in hindsight and uncertain in real time. The people who built wealth in those cycles were not the ones who waited for certainty. They were the ones who understood the thesis early, sized into the leaders, and held with conviction while everyone else debated whether it was real.

Tonight did not answer every question. Meta’s capex raise spooked the market. There will be more volatility. There will be more headlines about AI revenue misses and whether the spend makes sense.

But four of the most profitable companies in the world just told us they are spending more than ever on AI infrastructure and that the revenue is accelerating. The hyperscalers voted.

That is the signal. Everything else is noise.

Not investment advice. For educational purposes only. Do your own research.

If you want to go deeper, the weekly trading plan with specific setups, entries, and risk levels is available to paid subscribers.